{kind=link}

- Net Profits jump by a significant 58% YoY to reach to AED 1.3 billion.

- Robust balance sheet growth of 3% YTD reach AED 287 billion.

- Total income of over AED 3 billion, up 6% YoY.

- Strong growth in net operating revenues of 11% YoY to reach to AED 2.5 billion.

Dubai Islamic Bank (DFM: DIB), the largest Islamic bank in the UAE and the second largest Islamic bank in the world, today announced its results for the period ending March 31, 2022.

First Quarter 2022 Highlights:

- Significant growth in Group Net Profit of 58% YoY to AED 1,345 million vs AED 853 million last year. The strong growth was driven by lower impairments as well as a stronger top line growth.

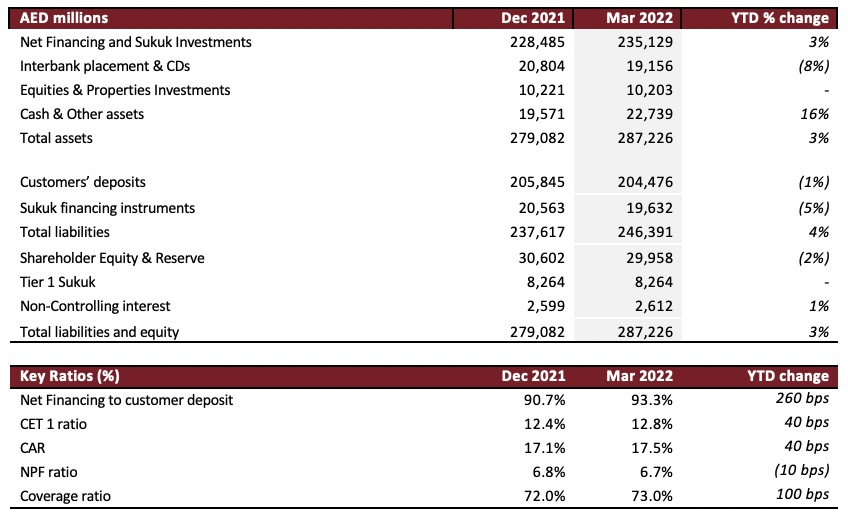

- Net financing and sukuk investments grew by 3% to AED 235.1 billion compared to AED 228.5 billion in 2021.

- Gross new financing of nearly AED 16 billion YTD driven by strong growth of wholesale bookings on the back of improved economic outlook.

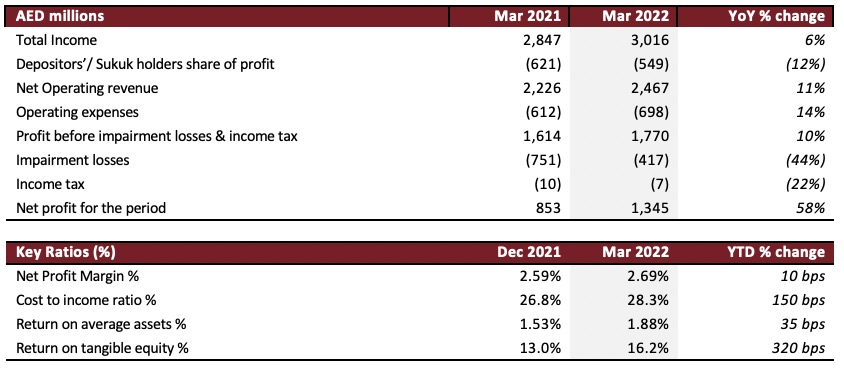

- Net Operating Revenues showed a robust growth of 11% YoY to AED 2,467 million vs AED 2,226 million in same period of last year.

- Steady growth of 6% YoY led to total income of AED 3,016 million compared to AED 2,847 million in Q1 2021.

- Net Operating Profit reached AED 1,770 million, a strong increase of 10% compared to AED 1,614 million in same period of last year.

- Strong balance sheet growth of 3% YTD to reach AED 287.2 billion supported by significant volume growth and new underwriting against improved operating conditions and recovering economic environment.

- Customer deposits remained steady at AED 204.5 billion with CASA increasing by 3.2% to AED 92 billion. CASA now forms 45% of the customer deposit base.

- Significantly lower impairment losses of 44% YoY to AED 417 million against AED 751 million in previous year demonstrate the improving asset quality.

- NPF ratio on a downward trend at 6.7% (-10bps YTD) compared to 6.8% in 2021, with absolute NPFs decreasing as well.

- Cost income ratio at 28.3% a rise of 150bps YTD. Operating Expenses increased by of 14% YTD now reaching to AED 698 million.

- Liquidity remains healthy with finance to deposit ratio of 93% and LCR of 123%.

- Continued healthy improvements on ROA now at 1.9% (+35bps YTD) and ROTE at 16.2% (+320bps YTD).

- Capitalization levels remain robust with CET1 at 12.8% (+40bps YTD) and CAR at 17.5% (+40bps YTD), both well above the minimum regulatory requirement. Total equity now stands at AED 40.8 billion.

Management’s comments for the period ending 31st March 2022:

His Excellency Mohammed Ibrahim Al Shaibani, Director-General of His Highness The Ruler’s Court of Dubai and Chairman of Dubai Islamic Bank

- Living in a rapidly evolving world and amidst ongoing international headwinds with a slower growth outlook, the UAE remains resilient growing from strength to strength with a forecast of over 4% for the year as per IMF. The continuous growth is a reflection of the UAE’s economic diversity and competitiveness which remains steadfast and on track to double the size of the country’s economy by 2030. The banking sector continues to demonstrate steady growth YoY as DIB’s Q1 earnings return back to pre-pandemic levels.

- Despite on-going unpredictable economic and international market conditions that are impeding progress, the bank’s total income of more than AED 3 billion reflects a 6% YoY growth and the balance sheet rising by 3% YTD reflecting its alignment towards the expansionary agenda of the UAE’s economy. DIB continues to transform into a more digital-focused and sustainable financial institution to future proof its business and unlock further growth opportunities in the market that will deliver stronger shareholder value in the years to come.

Dr. Adnan Chilwan, Group Chief Executive Officer

- DIB’s strong set of first quarter results with net profit growing by 58% YoY to reach to AED 1.3 billion is a demonstration of the bank’s ability to navigate through economic headwinds. I am pleased to state that we have successfully redefined our priorities in the post covid world with the launch of our new 5-year strategy at the beginning of the year. Supported by stronger operating revenue growth of 11% YoY and significant decline in impairments of -44% YoY, the bank’s financial position clearly denotes the resilience of the franchise and its inherent capability of withstanding market challenges.

- Our net financing and sukuk investments reflect a robust growth of 3% YTD to reach to AED 235 billion. This increase was supported by strong new underwriting and bookings during the quarter as part of the bank’s strategy to deliver balance sheet growth and target previously untapped customer segments. Our excess liquidity continues be utilized in building a high quality sukuk book earning a strong average return of around 4%.

- Persistent efforts on proactively managing credit underwriting and asset quality trends have led to NPF improving by 10bps YTD to reach 6.7%. We will continue to grow coverage over the period in the coming quarters to align with our guidance for the year.

- With a strong balance sheet and P&L growth during the period, our profitability ratios demonstrated healthy improvements with ROA now at 1.9% (+35bps YTD) and ROTE at 16.2% (+320bps YTD). The improving macro environment with higher oil prices coupled with rising rates will continue to benefit DIB where the majority of earning assets are in a floating rate book, aiding the bank in reaching its targeted margin guidance for the year.

Financial Review:

Income statement summary

Balance Sheet Summary

Operating Performance

The bank’s total income reached to AED 3,016 million demonstrating a growth of 6% YoY compared to AED 2,847 million in same period of last year following a more positive operating environment and improved business confidence. The improved sentiments were largely driven by recovering economic activities as a result of the successful hosting of the World EXPO 2020 and high vaccination rates. Net Operating Revenue had a solid growth of 11% YoY to reach to AED 2,467 million compared to AED 2,226 million last year.

Pre-impairment profit during the year increased by 10% YoY reaching to AED 1,770 million compared to AED 1,614 million. With prudent risk management and quality underwriting, the bank was able to achieve significantly lower impairment charges amounting to AED 417 million vs AED 751 million last year, an improvement of 44% YoY.

Operating expenses reached AED 698 million vs AED 612 million, with cost to income ratio now at 28.3%, still aligned to guidelines.

As a result, the bank’s Group Net Profit significantly grew strongly by 58% YoY to reach to AED 1,345 million vs AED 853 million.

Net profit margin increased to 2.7% (+10bps YTD) on the back of a rising rate environment with ROA and ROTE at a healthy 1.88% and 16.2% respectively.

Balance Sheet Trends

Net financing & Sukuk investments stood at AED 235.1 billion, a rise of 3% YTD from AED 228.5 billion in 2021. The bank witnessed a strong growth of gross new financing of nearly 16 billion YTD driven by robust growth in new corporate financing of nearly AED 12 billion and new consumer financing of AED 4 billion during the first quarter of the year. Sukuk investments saw an increase of 6% YTD to reach to AED 44 billion.

Customer deposits stood at AED 204.5 billion at the end of the first quarter with CASA increasing by 3.2% to AED 92.9 billion now representing 45% of deposits. Liquidity coverage ratio (LCR) at 123% remains well above regulatory requirement with finance to deposit ratio of 93.3% depicting a healthy and comfortable liquidity position.

Non-performing financing (NPF) ratio saw an improvement of 10bps YTD to 6.7% during the quarter indicating an improving asset quality position following strong risk management controls and improving economic conditions. The above has led to a Cash coverage ratio of 73% and overall coverage including collateral at 103% both rising by 100bps YTD. Cost of risk on gross financing assets continue to be on a downward trend and now stands at 69 bps compared to 99 bps in year-end 2021, an improvement of 30 bps during the quarter.

Capital ratios continue to remain strong with CAR now at 17.5% and CET 1 ratio at 12.8%, both well above the regulatory requirement.

Key Business Highlights

- DIB successfully issued a landmark USD 750 million 5-year Sukuk with a profit rate of 2.74% per annum. The deal represents the first Sukuk from the United Arab Emirates in 2022, paving the way for other issuers to access the international Sukuk market. DIB continues to be the leader in Islamic finance, with an established and strong investor following from Europe, Asia and the Middle East. Despite investor concerns around the global interest rate environment, DIB successfully priced its Sukuk with no new issue premium which is testament to the bank’s strong credit profile and sound business strategy.

- In line with the organization’s overall strategy, the Consumer Banking business launched the 5-year Customer Experience (CX) Strategy for 2022-2026. The strategy is based on 4 primary pillars namely (1) culture/mindset Shift (2) Inter-connected experiences (3) customer education and awareness and (4) measurement, insight and governance.

- DIB became an official member bank of UAE Trade Connect (UTC), a ‘cloud native’ solution running on Etisalat’s E1 Cloud, built around artificial intelligence capabilities. The technology provides DIB and other UAE banks with a decentralised, immutable, and completely transparent way of organising data that reduces the risk of fraudulent transactions. The benefits that UTC deliver will not only serve to protect DIB’s customers and the wider banking system but also enhance global trade. It is a milestone in the digitisation space that has the capacity to make trade financing more accessible, affordable and equitable. DIB is focused on providing value-added transaction banking solutions and look forward to supporting clients in the safest way possible.

- As part of DIB’s commitment to ESG, the bank has partnered with KFI Global, a leading provider of financial education for younger generations, to launch an intensive camping to own the financial education space in the UAE, especially for Gen Z. The aim of this strategic partnership is to allow teens and young adults (Gen-Z & Gen-Alpha) to insights and knowledge towards financial knowledge, behaviour and attitude which play a more important role in getting them to handle money smartly and responsibly. The partnership was established in line with the bank’s purpose to instil simplicity and convenience in its offerings. The successful campaign empowered over 2000 students, across 23 educational institutions with financial knowledge delivered over 205 hours of sessions, during the first quarter of 2022. The bank is dedicated to its commitment of inculcating financial literacy in the UAE youth and further generations to come.